I would say the HSBC fund as this includes exposure to the big tech companies in the USA. I would not consider ISWD myself as the performance hasn’t been great but it depends on whether you want exposure to world markets. I prefer the US market, but for some reason, the iShares ISUS product excludes the big tech names.

if you think sterling will weaken versus the US dollar then USD assets will get a boost in GBP terms i.e. if the choice is between a USD fund which is unhedged or a USD fund which is hedged into GBP then you would choose the unhedged one because that will benefit from GBP weakening vs USD.

quoted from Ramin

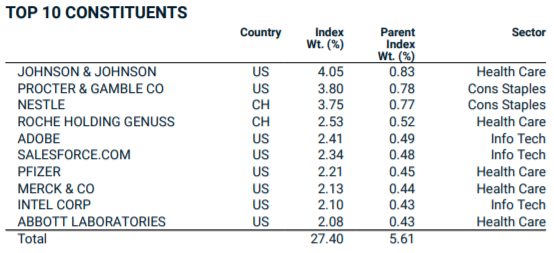

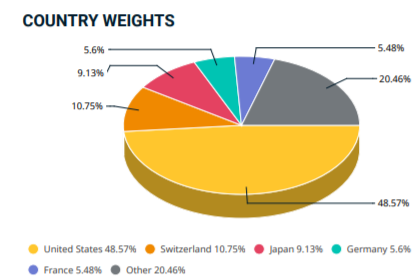

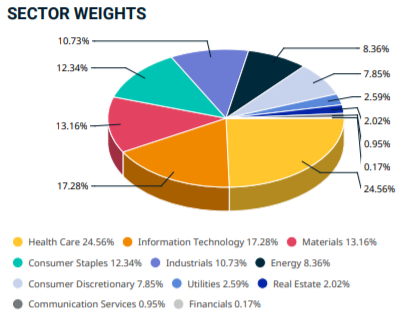

Overall i like HSBF fund over the Ishares MSCI. Dow Jones Titan 100 Index (HSBC fund) is biased towards US and Tech & Healthcare stocks which have been performing well and I believe both would probably continue to do so for a while in the long run. Though I would expect a short term correction coming to this fund as a result of likely rotation out of tech stocks to the heavily COVID battered stocks as we are seeing the progress on vaccines but I am still positive on its long term outlook - You may consider dollar-cost averaging if you do decide to go for this fund. I am a long term investor in this fund and don’t plan to do any funky stuff - probably will buy more if the market crashes .

Some details around both the funds for your reference if you are keen to understand this more:

MSCI World Islamic Index (USD): The MSCI World Islamic Index reflects Sharia investment principles and is designed to measure the performance of the large and mid cap segments of the 23 Developed Markets (DM) countries* that are relevant for Islamic investors. The index, with 366 constituents applies stringent screens to exclude securities based on two types of criteria: business activities and financial ratios derived from total assets.

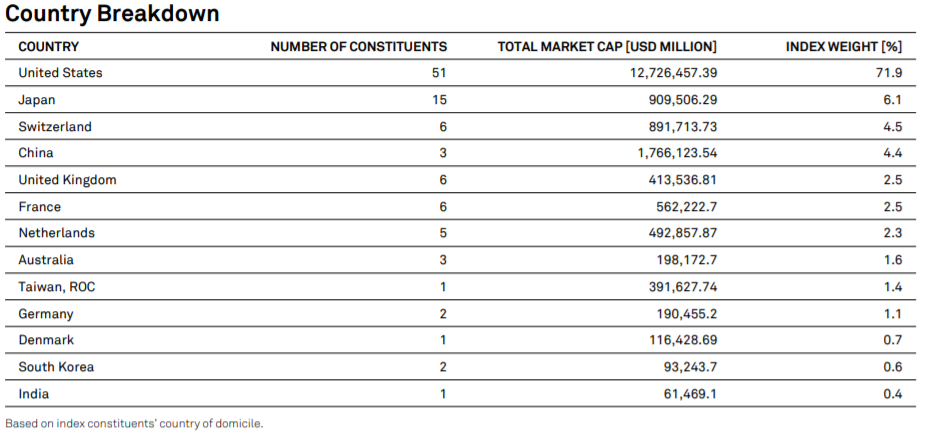

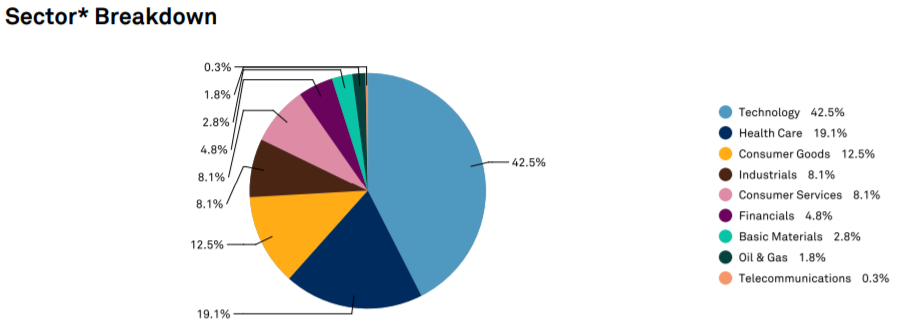

Dow Jones Islamic Market Titans 100 TR USD (i.e. HSBC Fund): The Dow Jones Islamic Market Titans 100 Index is designed to measure the performance of the largest 100 stocks traded globally that pass rules-based screens for adherence to Shariah investment guidelines.

The way it works is that as both the fund are global, underlying stocks are converted to either USD or GBP share class at “Spot rate”. As none of them is sterling hedged, you will have the currency risk regardless of which version you buy. However, it’s better to go for the GBP denominated fund as buying a USD denominated fund usually incur an FX charge of ~1% from the platform provider.

Agreed that the literature of the fund says that there can be an entry charge of up 5.54% but its generally waived as FCA frowns upon the entry charges. I have spoken to AJ bell on this at length and have been assured that this does not apply to the fund on their platform - for my peace of mind, I invested a minor amount to see if there was any deduction along the lines of 5% and it did not. Suggest to do the same for your peace of mind too.

This does not apply here as both the funds here are “unhedged”.

Ramin did say that if the fund is sterling hedged, it will be very obvious with the word “hedged” in the literature .

The fact that a fund, having underlying assets in USD being translated to GBP share class on spot rate does not make it a sterling hedged.

The HSBC fund is domiciled in Luxemburg and the stamp duty does not apply to it. Don’t think the stamp duty apply to funds in general… The fund would probably be paying it when its trading in it…

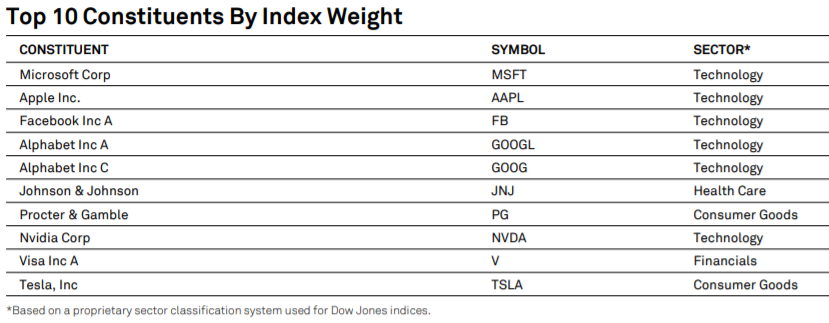

Just want to highlight again that one should look at the stocks listed in the fund e.g. Apple is listed in US and have the USD denomination. the GBP fund which is unhedged will simply convert the USD value of Apple to GBP on spot rate. Stamp duty is probably be linked to where the fund is listed not the currency it is denominated.

Japan is looking cheap and attractive at the moment but yes we are limited to shariah funds availability although the indices are there - investment companies need to launch them.

That was very useful. I am now more inclined now to go for the HSBC fund. As you suggested, using the dollar cost averaging strategy is the way to go to reduce the risks during these uncertian times. I think AJ bell have a pretty decent dealing charge of £1.50 for every purchase which is good.

Im more inclined as well after reading this to put my money in the HSBC fund for couple of reasons,

1- for the fact its a fund and not an ETF

2- its accumulating and not a distributing fund which would be better on the long run

3- A lower expense ratio of 0.49% in comparison to the MSCI world of 0.60%

My only doubt is that whether i prefer Dow Jones over the the more distributed globally the MSCI.

At the same time i can imagine Warren Buffet looking at me and saying why are you even thinking twice? just put your money in the S&P500 ! lol but sadly we don’t have reasonable islamic one tracking the S&P500 except for Wahed.

@Zeeshan does AJ bell allow to start investing with less than a 1000 k in the HSBC IC ?

What difference does it make of it being ETF or Fund - just the live and close of day valuation - why does that has to be a consideration? what am I missing?

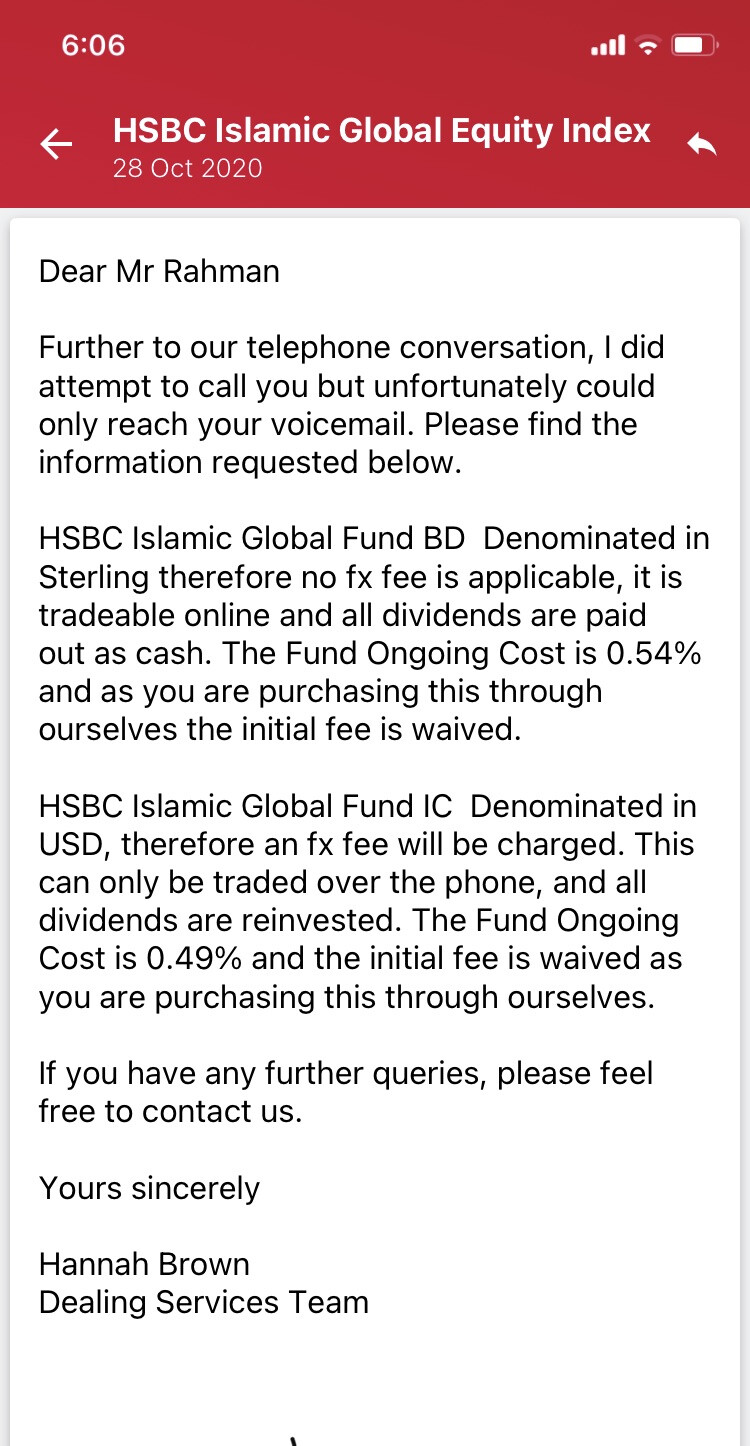

So be aware that AJ bell have two share classes:

“IC” which is accumulating but its actually a USD share class - I know the price on their website is showing it in GBP but its wrong and they are trying to sort out and hence it trading via app/website is locked. YOu will have to call them to buy. So the point to consider is that as its a USD share class, you will incur a oneoff 1% FX fee from AJ bell on Buying and then again on selling. Something to be aware.

“BD” is the GBP denominated version but to your dislike its a distributing fund . As I have said before you can simply reinvest the dividend @£1.5 per transaction and can save a total of 2% oneoffs (this is not ongoing charge).

HSBC will actually cost you slightly more in the end as 0.54% fund fee + 0.25% AJ bell fee = 0.79% VS 0.6% MSCI on Trading 212 ISA so no platform fee.

Do istakhara - I agree on principal that the more broadest the index the better it is but personally feels HSBC may do well (not a recommendation at all).

Dont Think Wahed ETF is tracking S&P 500 but FTSE shariah index and they have 200 constituents - you cant buy US ETF in UK anyway so that is out of the picture.

No minimum investment probably at least 1 share as I don’t think they do fractional share selling.

Speaking of Sukuks, I’ve come across the BNP PARIBAS ISLAMIC FUND HILAL INCOME - USD.

Its actively managed with several classes, ill do more reading about it but from what i read briefly its not a bad option so far and its available on AJ BELL as well.

yes that is fund fee but don’t forget that AJ bell will charge you 0.25% on top of whereas if you buy MSCI via Trading 212 ISA - no additional fee in addition to fund fee.

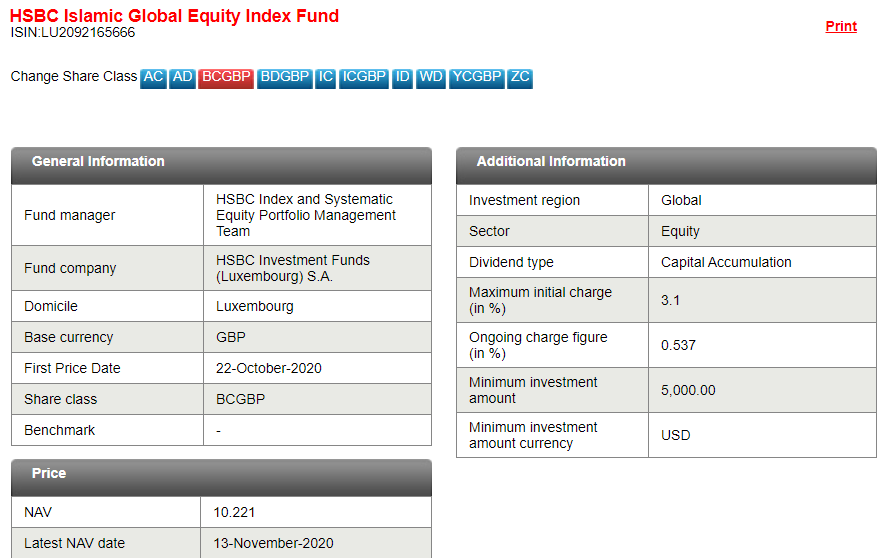

Seems like HSBC have just started the GBP accumulation version couple of weeks ago as “BC” share class. - Worth giving a call to AJ bell to see if they can add it to their offering.

Im not sure why im still afraid of opening with trade 212 , for some reason i don’t feel comfortable using it for a long term investment

I called them, they don’t think they will be adding any other classes to what they have already for some reason, i’m now looking for all other brokers to see where its available.

.

.