I am planning to change my pension to the Sharīʿah fund that is available to me. This fund is the “HSBC Islamic Global Equity Index Pension Fund” which has been confirmed as Sharīʿah compliant here and here.

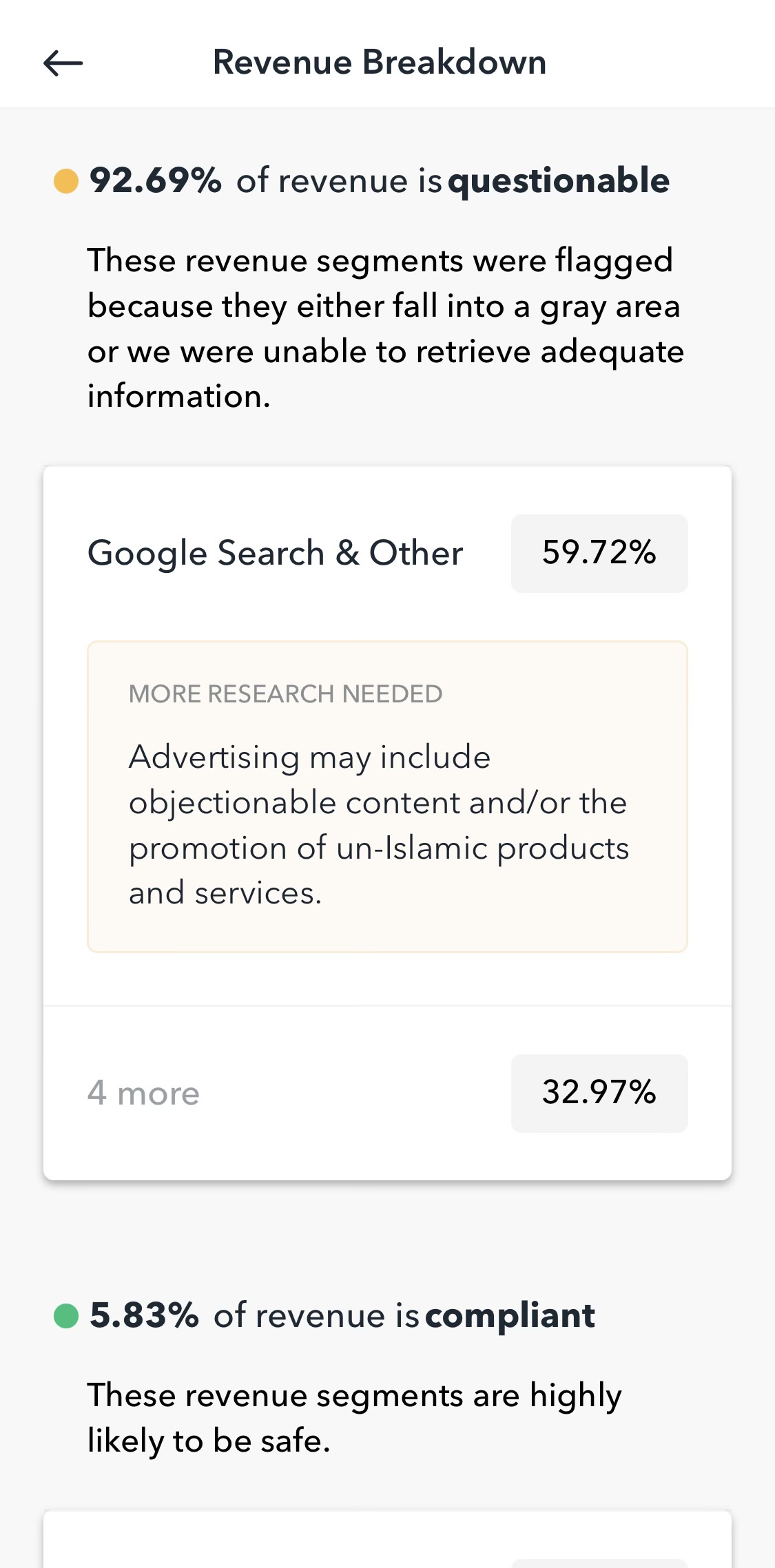

My question is that in the top 10 holdings of this fund, half of them are deemed as ‘Questionable’ by Zoya - Apple, Microsoft, Alphabet Inc - CL A and CL C and Facebook (I’ve added screenshots of each Zoya page). What is the reason for this and which ruling is best to follow? If I was to follow the pension fund ruling then that would mean that those particular stock are halal to invest in and I can do so on my personal investments (I’ve been avoiding them based on the Zoya ruling). Am I correct in this thinking?

The fact sheets are available here and here (the second fact sheet has both classes of Alphabet which is why I included both in the above paragraph).

As @Mufti_Faraz_Adam alluded, there are nuances in screening methodologies which can lead to different conclusions in shariah compliance. It looks like the HSBC fund you’re referring to is based on the Dow Jones Islamic Market Global Titans 100 Index. While the Dow Jones Islamic methodology is largely based on the AAOIFI standards, there are some differences in how they are interpreted by their respective shariah board. You can read about their methodology in more detail here (page 29) and ours here if you’d like to compare them side-by-side.

Regarding the “questionable” status that you see in Zoya—this typically refers to revenue segments that fall into a grey area where there might be a difference of opinion among scholars. For example, Google and Facebook primarily earn their revenues through advertising. While there isn’t anything inherently wrong with advertising, it’s important to note that the nature of those ads may be of objectionable nature or they may promote un-Islamic products/services. Instead of outright labeling them as non-compliant, we’ll flag such revenue segments as questionable instead so that you can make your own decision based on your own research and personal preference. We do our best to highlight this as clearly as possible on the detailed compliance report screen.

That being said, there’s no right or wrong answer here. We understand and respect that there will always be varying scholarly opinions on such topics. Our goal with Zoya is to empower you with the tools and information you need to make conscious investment decisions without compromising your faith.

For the majority of workplace pensions based in the UK, the only Shariah compliant pension offered is the ‘HSBC Islamic Global Equity Index Pension’, this is from my personal experience working at firms which have either used the Scottish Widows or the Aegon pension scheme (maybe someone can confirm this or relate their own experiences).

@Mufti_Faraz_Adam Now a question which arises because of this grey area mentioned, is there any further reading or views you can share from the Hanafi madhab for example that would support/negate the consumption of this particular pension scheme?