I agree with Zeeshan in that the key variable is the platform fee which is where you can save.

However, as this thread probably indicates, Zeeshan you’re actually a very switched-on investor who understands the underlying mechanics of where your money is being deployed and how. You are also fairly interested in investing (at least to the extent that you’ve done a decent bit of research).

My experience is that many Muslim investors are not at this level of sophistication and so the choice becomes not only about platform fees but about user experience/ease etc. Here Wahed (and other roboadvisors) have a slight edge as you just have to create an account and choose your risk preference and pay in and you’re done. With AJ Bell as a Muslim investor there isn’t a cookie cutter portfolio done for you. So you have to do all the Wahed steps plus you have to search a few Islamic funds and set up direct debits to them etc. Not rocket science and something pretty much everyone can do within an afternoon of focused reading - but surprisingly few people do.

So, as we’ve always said at IFG - AJ Bell and DIY approach is always cheaper - but it may not get you the professional portfolio construction, the diversification of different funds, and it will mean a bit more legwork your end.

Jazak Allahu Kahiran @Musa_Absi. I understand and accept what you are saying and as @ibrahimkhan mentions, you can buy some of the funds yourself and look to replicate our models should you have the time, knowledge and inclination to do so.

It may be worthwhile pointing out again that we are not a fund. Each model we offer is a collection of different funds across asset classes and the weighting of each will differ according to their risk profile. We charge for managing that collection of funds on the clients behalf. In addition, we are a start-up investment firm who do not have the assets under management and therefore cannot benefit from the economies of scale that the likes of AJ, HL or Vanguard have. However, with the help of fellow Muslims by investing with us we aim to offer a similar, if not better, service in the future. That has always been Wahed’s aim.

Having seen what was available in the market, Wahed was created with the view to help the mass market Muslim community to save into a shariah compliant investment platform where their investments are managed to ensure that it is risk appropriate to their needs but most importantly, it remains halal in their hands through the issuance of the purification reports also. We firmly believe that no other global firm is doing this right now.

Barak Allahu Feekum for your thoughts and I pray that my comments help also.

Jazakallah @ibrahimkhan. I am humbled. Thank you for your kind and generous words.

I can’t agree enough with your assessment. All of us need to learn more about investing before deploying huge sums of money. It looks to me that we have a tendency of buying a posh car without knowing how to drive it - after the obvious result some of us just move away from investment and that is not good for the Muslim community. We all need to learn and become smart investors (Iqra).

I am so impressed by the work you and your team are doing in this area. This will help the community a great deal - Thanks. I would like to make a small contribution to this journey and have started a thread on Financial Education: Investment TIPS for Absolute Beginners that I am hoping would be helpful for some.

Jzk for all your efforts, as well as the IFG guys. I have learnt a great deal so may Allah SWT reward you all. Ameen

I had a few of questions:

Is there a cheaper platform for fees for Stocks & Shares ISA which invest into the HSBC Islamic fund other than AJ BELL (not T212)? If only Vanguard did Shariah compliant funds!

Can you invest in 2 funds in one ISA Account? If so, do you get hit with two fund charges?

What are the pros/cons of investing in the div reinvested vs div distributed funds?

Like you, my pension with Standard Life is also invested in the HSBC Islamic Fund. Therefore, would opening a Stocks & Shares ISA with the HSBC fund not be a good diversifying strategy?

Glad to hear that you are finding this community helpful.

I am not aware of any other platform offering this fund at a lower platform charge then 0.25%. This is not to be confused with the fund charge which is generally around 0.5% that i have seen at most place. Let me know if you do come across with a lower fee anywhere. (T212 does not offer funds so this is not available on it)

You can invest in how many funds and stocks in an ISA account. What you may be confusing is that you cannot open more than 2 Stock and shares ISA in one tax year but there is no limitation of a number of holdings in the ISA account.

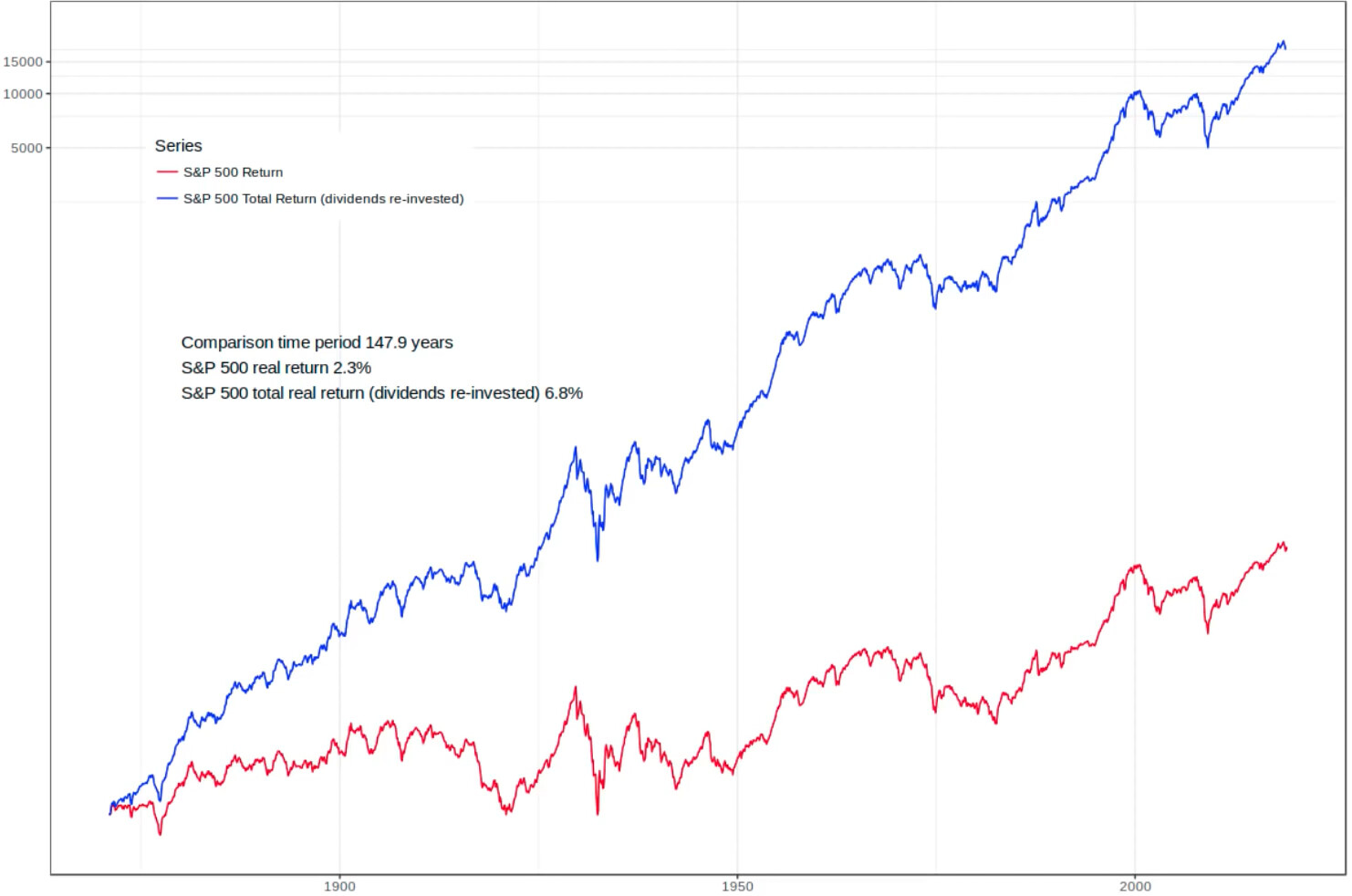

Dividend reinvestment simply means that whatever dividend you receive, you would reinvest them rather than using it. compounding effect of dividend reinvestment is unbelievably powerful. See below screenshot showing a 147 years history for gains with (blue line) and without (red) dividend re investment.

Now to your question, there can be two versions of the same fund one which is paying a dividend and other which automatically reinvesting dividend also known as accumulation funds. AJ bells offer HSBC fund in both classes but accumulating fund is being offered in USD currency which will incur a 1% fx charge from AJ belle when you invest and divest in it. The dividend-paying fund is in GBP and pays dividend half-yearly I think (pls check). Personally, i would invest in the GBP fund to save the 1%+1% FX charge and would just manually reinvest in the same fund whenever dividend is recevied.

Difficult to comment - maybe yes considering the fund itself has approx a holding of 100 shares VS MSCI Ishares but the shares within it are all growth stocks which have been performing brilliantly for past few years and my personal view is that they would probably continue to grow for some time. (Just my view). you may find this thread useful : Selecting an ETF

PS: for your pension, you should also check that the fee you are paying with standard life is lower than what you could pay to AJ Bell within SIPP i.e. 0.79% total (HSBC fund fee 0.49% + AJ bell platform fee 0.25%). If you are paying more then this then worth considering opening a SIPP with AJ bell and transfer your pension with them.

Hope above is helpful - feel free to ask any further questions.

Jazakallah for your swift response brother Zeeshan,

Yes, from doing all my research I also found AJ BELL to be the cheapest for fees. Will let you know if I come across a cheaper one.

So with multiple funds in one S&S ISA, wouldn’t that mean multiple fund charges to mange each fund? For example, 0.5% on one fund and 0.5% on another fund would be a total of 1% fund charge on your total investment? As I was thinking of investing into the HSBC & ISHARES in one S&S ISA but the total fund charges will be quite high.

Yes, I read your point about the FX fee earlier and was also leaning towards the GBP fund for the very same reason. The positive also being that dividends are tax free with a S&S ISA. Therefore, the BD GBP fund would be my preference too.

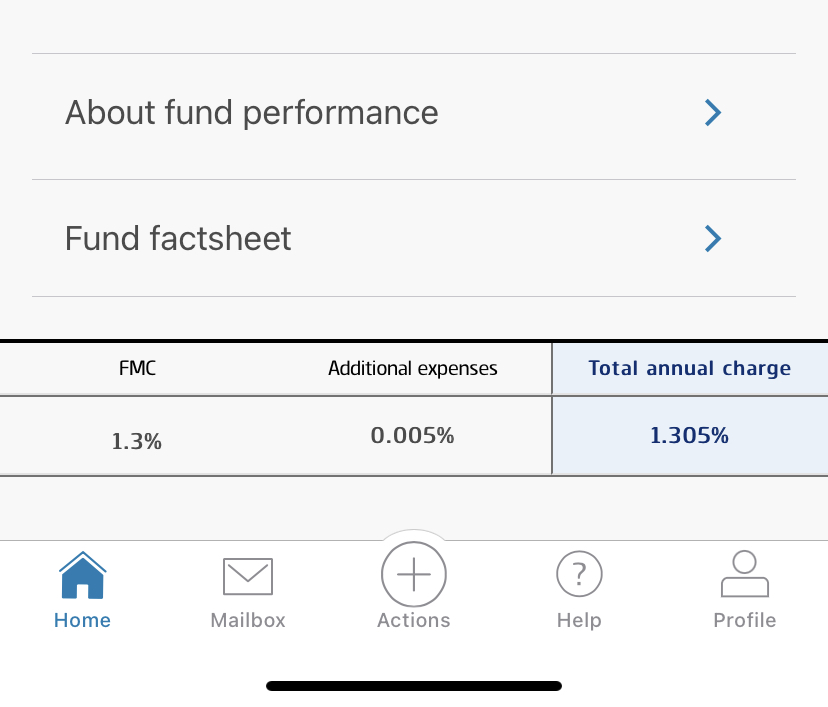

Very good point on the SIPP. I’ve checked and Standard Life are charging annual 1.305% - high because it’s a previous employer pension in which no payments are being made into it (screenshot below):

I am now on a DB Pension with my current employer. However, my current employer is switching to DC in the next couple of months so was going to wait and transfer my Standard Life Pension to my current employer pension (which will be Legal & General who also have a shariah compliant pension fund). And of course, the fees with my current employer should be less than my Standard Life Pension as it’s with a current employer who will contribute. Does that make sense?

it does not work like that. So if you invest £1000 in one fund, the 0.5% charge, for example, the charge will be £5. If you invest the £1000 as £250 each in 4 funds, then the total charge would still be £5 (£250*0.5% = £1.25 X 4 funds) - Its the amount of investment that the charge is applied not the number of funds.

Anoying - a lot of platforms are charging insane amounts for this funds.

Definitely - move that out of standard to Legal and general. My pension is also invested with legal and general and they have the best rates for this fund. I am on the “WorkSave generation 3” pension scheme with L&G and the fund charges for HSBC is only 0.35%. The platform fee is very minimal but that is a special negotiated employers rate.

The fund charges are what they are - its does not matter if the employers contribute or not. However, if your employer run a matching scheme, make most of it. Also, a side tax tip, if you are a high tax rate payer, make sure you claim the additional tax relief on your annual tax assessment.